Axon Enterprise: Taser Empire or Overhyped? The $20B Tale...

Is this the next best bet?

Business Profile

Name: Axon Enterprise, Inc. (AXON)

Industry: Public Safety Technology

Market Cap: $20+ Billion

Price: $250.43

Exchange: NASDAQ

Founded: 1993, headquartered in Scottsdale, Arizona

CEO: Rick Smith

What’s The Story Behind Axon Enterprise?

The story behind Axon Enterprise is a compelling evolution from a niche stun-gun manufacturer to a mission-driven public safety technology powerhouse. It’s a story of innovation, purpose, and smart reinvention. Founded by Rick Smith, originally as Air Taser, Inc., in response to the tragic shooting of two of his high school friends.

The goal: Create non-lethal weapons as alternatives to firearms. He views Axon not as a weapons company, but as a public safety tech company on a mission to reduce violence, increase transparency, and modernize policing. In 2017, TASER International rebranded as Axon Enterprise to reflect its broader mission: empowering public safety through connected technology.

Source: Axon Enterprise Investor Relations Presentation 2024

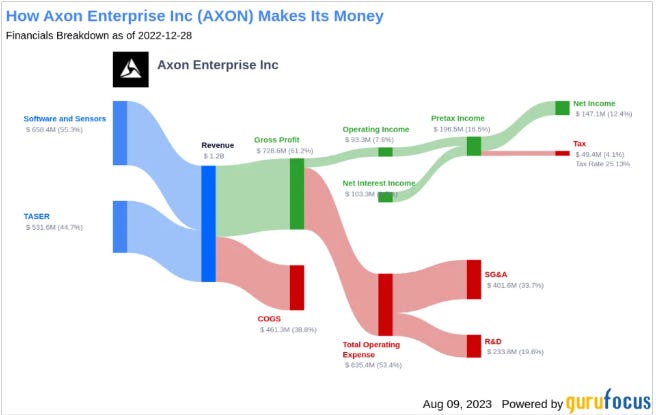

How Does Axon Enterprise Make Money?

Axon is a global leader in public safety technology, transforming how law enforcement agencies operate worldwide. As the premier provider of non-lethal defense solutions, Axon has built a powerful ecosystem that extends beyond hardware into cloud-based digital solutions and AI-driven analytics. With its presence spanning North America, Europe, and beyond, Axon plays a pivotal role in modernizing policing and public safety.

Axon’s revenue is fueled by a multi-faceted business model that combines hardware sales with high-margin software and subscription services. The company generates income through:

TASER Energy Weapons: A cornerstone product used by law enforcement agencies worldwide.

Axon Body-Worn Cameras & In-Car Systems: Essential tools for accountability and officer safety.

Axon Evidence (Cloud Software): A digital evidence management platform with recurring subscription revenue.

Axon VR Training & AI Solutions: Cutting-edge technology that enhances officer preparedness and decision-making.

By integrating hardware with SaaS-based solutions, Axon has created a highly scalable and profitable business model. As public safety agencies continue their digital transformation, Axon is positioned to drive sustained long-term growth and industry leadership.

Source: Axon Enterprise Investor Relations Presentation 2024

Does Axon Enterprise Have a Big Competitive Advantage Around the Business?

Axon Enterprise has built a formidable competitive advantage through its integrated technology ecosystem, long-term contracts, and innovation in public safety solutions. These factors position it as the market leader in law enforcement technology.

Axon maintains a strong competitive edge through its technology-driven approach, extensive product portfolio, and recurring revenue model. Key advantages include:

Integrated Hardware & Software Solutions: Axon seamlessly integrates TASER devices, body cameras, and cloud-based evidence management, creating a unique end-to-end platform that competitors struggle to replicate.

First-Mover Advantage & Brand Trust: As a pioneer in non-lethal defense and digital policing, Axon has established strong relationships with law enforcement agencies worldwide.

Recurring Revenue Model: High-margin subscription services for digital evidence management ensure stable and predictable long-term revenue. In the fourth quarter of 2024, Axon Enterprise’s recurring revenue — primarily driven by software and subscription services—accounted for roughly 40% of the company’s total revenue and 95% of its revenue is tied to customers on subscription plans. A 123% revenue retention rate demonstrates strong customer satisfaction and indicates that customers are purchasing more of Axon’s products.

Strategic Contracts & Government Partnerships: Axon secures multi-year contracts with law enforcement agencies, ensuring consistent revenue streams and high client retention.

High Barriers to Entry: Advanced R&D capabilities, regulatory approvals, and deep integration into law enforcement agencies make it difficult for new players to enter the market. In

Investment in AI & Public Safety Innovation: Axon is at the forefront of AI-powered policing tools, VR training, and real-time analytics, keeping it ahead of industry trends.

With its strong financial position, relentless innovation, and deep market penetration, Axon is well-positioned for long-term leadership in public safety technology.

Moat: Axon Enterprise has a strong competitive moat based on several key factors:

Why Axon’s Moat is Durable: Axon Enterprise has built a durable competitive moat by combining industry-leading hardware, proprietary software, long-term contracts, and deep integration into law enforcement workflows.

Does Axon Generate a High Return on Capital?

Axon Enterprise’s capital allocation is relatively weak. Historically, Axon Enterprise has struggled with capital allocation, as shown by five-year averages of:

ROIC: 3.2%

ROE: 7.9%

ROA: 3.9%

However, recent years show signs of improvement:

ROE: Negative in 2021, rising to 19.1% by 2024

ROA: Negative in 2021, moving up to 9.6% in 2024

ROIC: From a loss in 2021 to 10.1% in 2023, dipping to 3% in 2024

Capital Allocation Highlights

Return on Equity (ROE):

Climbed from negative territory in 2021 to an impressive 19.1% by 2024.

Suggests rising confidence in

how Axon deploys shareholder funds.

Return on Assets (ROA):

Shifted from negative in 2021 to 9.6% in 2024.

Indicates improved efficiency in turning assets into profits.

Return on Invested Capital (ROIC):

Jumped from a loss in 2021 to 10.1% in 2023, then dipped to 3% in 2024.

May reflect heavier investments or acquisitions not yet yielding full returns.

Does Axon Enterprise Have Favorable Long-Term Growth Potential to Reinvest Capital and Scale?

Axon Enterprise is well-positioned for long-term growth, leveraging strong cash flows, strategic product expansion, and a growing market for law enforcement technology. While it continues to scale its core business in body cameras and less-lethal weapons like tasers, its investments in software, cloud-based services, and AI technology provide additional growth opportunities. With a focus on capital efficiency and long-term partnerships with government agencies, Axon has the potential to reinvest capital effectively and scale in a rapidly evolving public safety landscape.

Source: Axon Enterprise Investor Relations Presentation 2024

With long-term contracts with law enforcement agencies, a strong reputation for innovation, and integrated operations across hardware and software solutions, Axon ensures stable revenue and profitability. Additionally, its strategic investments in AI, data analytics, and cloud technology position it for long-term success as the market for public safety technology continues to grow. This combination of scale, innovation, and adaptability gives Axon a durable competitive advantage in an evolving industry.

Massive Market Opportunity

The chart highlights a $129B Total Addressable Market (TAM), showing Axon’s expansive growth potential, with under 15% U.S. law enforcement penetration — indicating a vast untapped customer base. Key segments like digital evidence management, TASERs, body cameras, and AI solutions each contribute significantly to this TAM. Given that many agencies, especially smaller ones, often lag in adopting modern tech yet face rising demands for accountability and efficiency, Axon seems well-positioned to fill these gaps. From my perspective, helping smaller departments upgrade and streamline processes can have an outsized impact, suggesting plenty of room for Axon to expand both domestically and globally. However, if we look at the market share of what Axon actually owns, its relatively a small share of the market with 1.6%.

Source: Axon Enterprise Investor Relations Presentation 2024

Key Growth Drivers:

Expanding Product Ecosystem: Axon’s suite of products, from body cameras to tasers and software like Evidence.com, is deeply integrated, creating a long-term customer lock-in. As law enforcement agencies increasingly adopt its technology, the network effect grows, driving recurring revenue through SaaS offerings.

Government Contracts: Axon’s long-term relationships with government agencies provide a stable revenue stream, with many contracts involving multi-year agreements that reduce exposure to short-term market volatility.

Data and AI-Driven Services: Axon’s shift toward AI-powered tools for public safety, including automated video analysis and predictive policing software, positions the company to benefit from the growing demand for data-driven decision-making in law enforcement.

Software and SaaS Growth: With a focus on recurring subscription revenue from cloud-based services, Axon is diversifying its revenue streams. As more agencies rely on Axon’s software for data storage, analysis, and management, the company can scale its operations further.

Expansion into International Markets: Axon’s global footprint, though currently concentrated in North America, has room to expand internationally. As more countries modernize their law enforcement practices, the company can scale by capturing market share in new regions.

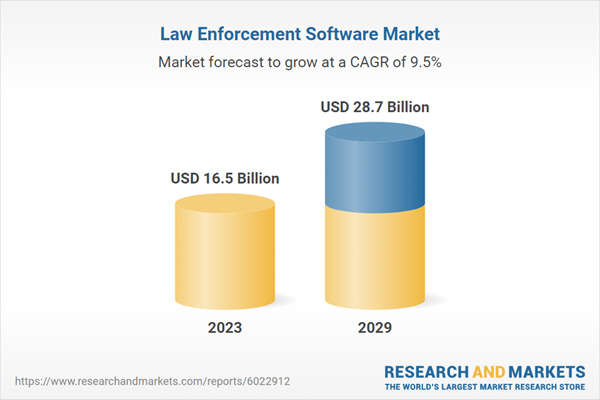

The public safety technology market is projected to climb from USD 16.5 Billion in 2023 to USD 28.7 Billion by 2029, reflecting a strong 9.5% CAGR driven by digital solutions in law enforcement: (1) agencies are embracing data analytics, body-worn camera software, and incident management tools; (2) heightened public focus on accountability fuels continuous innovation; and (3) expanded budgets create fresh opportunities for tech providers.

While the technology landscape is rapidly evolving, Axon’s ability to stay ahead of trends, innovate with AI, and maintain long-term contracts with government entities positions it to continue growing and expanding its footprint in the public safety technology sector.

How does Axon Enterprises’ Stock Performance Compare?

Axon has shown resilience in a dynamic and rapidly evolving market, outperforming many tech peers with consistent growth, strong recurring revenue, and solid institutional backing.

Institutional Support & Expansion: Major investors include Vanguard, BlackRock, and Fidelity, signaling strong confidence in Axon’s long-term business model and public safety leadership.

Stock Performance: Axon’s stock has delivered double-digit gains in 2024, driven by expanding adoption of its cloud software, AI solutions, and global law enforcement contracts.

Revenue Growth & Stability: While not a traditional dividend payer, Axon prioritizes reinvesting in innovation and scaling recurring revenue streams, with revenue consistently growing 20–30%+ year-over-year — reflecting strong demand for integrated public safety solutions.

If we compare AXON to peers in defense tech and SaaS, it's consistently outpaced most in both revenue growth and total return. Only a few niche AI players have matched its performance over the last three years, and those often lack Axon’s combination of profitability, institutional contracts, and scalability.

Is Axon Enterprise Run by Exceptional Management with High Insider Ownership?

Source: Axon Enterprise

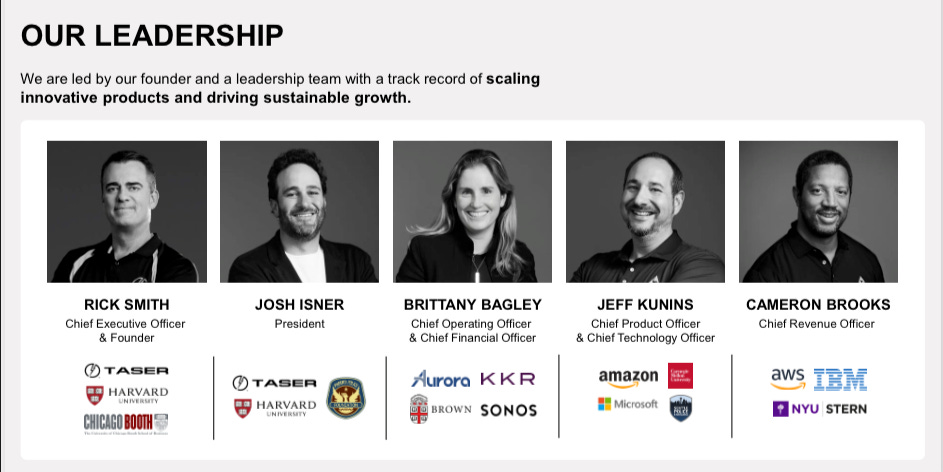

Axon Enterprise's leadership team, led by CEO Rick Smith, has been instrumental in shaping the company into a leader in law enforcement technology, particularly with its body cameras and less-lethal weapons, like tasers. Rick Smith, who co-founded the company and has served as CEO since 2000, is recognized for his visionary approach to technological innovation and his commitment to transforming public safety. Under his leadership, Axon has made strategic moves that blend both technological advancement and social responsibility.

Key Management Strategies:

Innovation & Product Development: Rick Smith has focused on creating an integrated suite of products, from the Taser to body cameras and cloud-based software like Evidence.com. This emphasis on product development has enabled Axon to dominate the law enforcement technology market.

Mission-Driven Leadership: Rick Smith’s leadership is guided by a mission to “protect life” and improve public safety. This purpose-driven approach is central to Axon’s identity and resonates with the company’s customers, particularly law enforcement agencies.

Expanding the Ecosystem: Beyond hardware, Axon has strategically expanded into software and data management solutions, creating a comprehensive ecosystem that locks in customers and makes it difficult for competitors to replicate.

Long-Term Vision: Smith has consistently demonstrated a long-term focus, seeking to modernize law enforcement practices and lead the industry in technology adoption. Axon continues to innovate with initiatives such as artificial intelligence for public safety and expanding its cloud-based offerings.

Adaptability: Axon has proven adaptable to changes in law enforcement needs and technology trends. For example, its shift towards AI and software-based solutions allows it to remain ahead of competitors in an evolving market.

Insider Ownership and Alignment with Shareholders: Rick Smith, as the co-founder and CEO, holds a substantial ownership stake in Axon 4% worth $1.8 billion, demonstrating his deep commitment to the company’s success and aligning his interests with long-term shareholder value. However, compared to some companies, insider ownership at Axon is not overwhelmingly high, as much of the company’s shares are held by institutional investors and the public.

Here is a closer look at insider ownership:

Rick Smith, CEO and co-founder, holds a 4.95% significant number of shares, reflecting his strong personal investment in the company's success.

Other executives and key employees also have equity stakes, ensuring that the leadership team remains incentivized to drive long-term value.

While insider ownership is meaningful, it is not at the level of some privately held companies or those with dominant insider stakes. However, the company’s alignment between leadership and shareholders remains strong due to the leadership’s ongoing involvement and long-term focus on growing Axon’s ecosystem.

Source: Finchat

Source: Axon Enterprise Investor Relations Presentation 2024

Has Axon Enterprise Created Value for Shareholders in the Past?

Axon Enterprise has consistently created significant value for shareholders through a combination of strong revenue growth, strategic reinvestment, expanding profit margins, and a sharp focus on recurring revenue streams. Here’s how:

📈 Stock Performance

Axon’s stock has delivered impressive long-term returns. Over the past 5–10 years, it has outperformed broader indices like the S&P 500, driven by strong fundamentals and market leadership.

In 2023–2024 alone, Axon’s stock posted double-digit percentage gains, reflecting investor confidence in its innovation and long-term contracts.

💰 Revenue & Profit Growth

Axon has grown revenue at a 20–30% CAGR (Compound Annual Growth Rate) in recent years, fueled by increasing adoption of TASERs, body-worn cameras, and its Axon Cloud platform.

Gross margins have improved steadily as the company scales its software-as-a-service (SaaS) offerings, which are higher-margin than hardware alone.

🔁 Recurring Revenue Model

Axon has transitioned from a product-based model to a subscription-based model, especially through Axon Evidence, Axon Cloud, and Axon Records.

As of recent filings, over 75% of revenue is from software revenue over 5 years or tied to multi-year contracts, providing financial visibility and stability.

👥 Shareholder Alignment

CEO and founder Rick Smith holds a meaningful equity stake, aligning leadership with shareholder interests.

The company doesn’t pay dividends, opting instead to reinvest in R&D, product development, and international expansion, which has driven long-term compounding.

Axon vs. Vanguard S&P 500 ETF: A Performance Check

Axon Enterprise has outperformed the Vanguard S&P 500 and other major indices in terms of stock growth, driven by its leadership in the public safety tech space, its successful shift to recurring SaaS revenue, and its innovative product suite. While Axon’s stock has outperformed, it has also been subject to higher volatility, given its position in a niche market. This could impact risk-adjusted returns relative to broader indices like the S&P 500, which tend to be more stable due to diversification.

Axon Enterprise’s Capital Reinvestment — Strategic, Growth Focused!

Axon Enterprise is not operating with minimal capital reinvestment. It is strategically reinvesting capital to fuel growth, advance technology, expand its global footprint, and maintain a competitive edge in the public safety sector. The company’s consistent capital reinvestment into innovation and scaling efforts is central to its growth trajectory.

💰 CapEx Snapshot (2024)

CapEx: ~$78.79 million

Free Cash Flow: ~$329.53 million

CapEx/Revenue: -0.37%

CapEx/Operating Cash Flow: 0.2%

📌 What It Means

Lower CapEx/Revenue at -0.37% → Axon is heavily investing in capital-intensive projects relative to its revenue → Could signal a more cautious approach to growth rather than a pragmatic approach.

CapEx/Cash Flow at 0.24% → Axon is focusing on maintaining strong operating efficiency. → Suggests modest growth focused approach.

⚖️ Why It Matters

A lighter reinvestment load gives Axon flexibility — more cash for dividends, buybacks, or future bets.

But if underinvestment drags on, it could slow growth long term.

💬 My Take

Axon’s capital reinvestment strategy appears to be growth-focused but prudent, investing selectively in high-return areas while ensuring operational efficiency and maintaining a solid cash flow. It’s a balanced approach, signaling long-term sustainability without overextending itself.

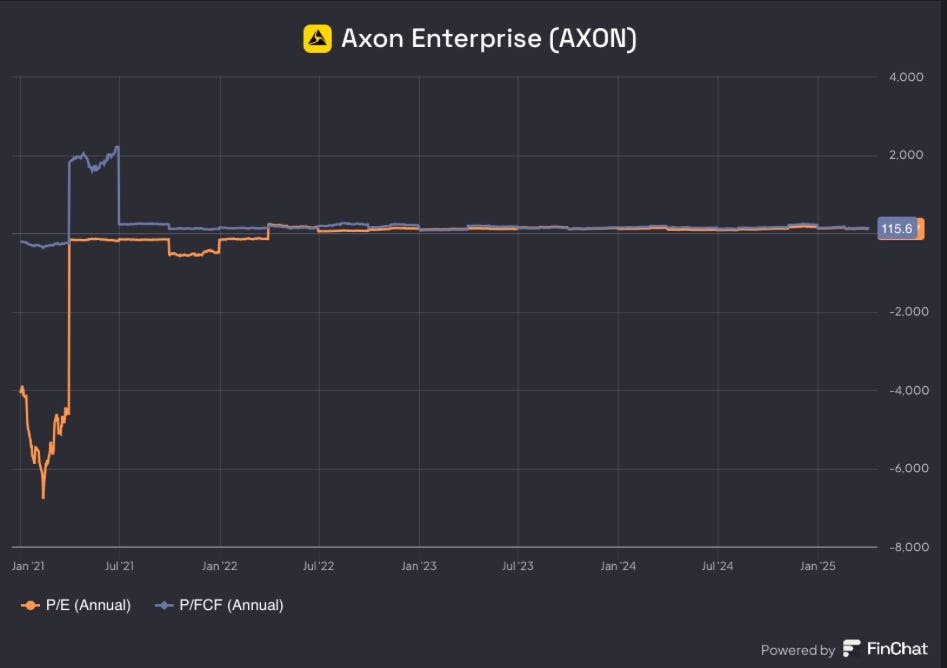

Does Axon Enterprise Valuation Provide a Margin of Safety?

DCF forecast: 8.01% free cash flow growth annually for the next 10 years

Past 5-year FCF growth: 15.8% CAGR

Valuation multiples:

P/FCF: 115.6x

P/E: 112.4x

What This Tells Us

That investors expect significant future growth in Axon’s cash flows and earnings.

The high multiples indicate that investors have confidence in Axon’s future performance, especially in terms of cash flow generation and profitability.

But Here’s the Thing

If you believe Axon can continue to innovate and maintain its leadership in public safety tech—especially with its cloud solutions and AI capabilities → This could be a mispriced gem.

P/FCF and P/E might seem high, but for a company with a dominant position and growing recurring revenue, these multiples could still be reasonable.

You’re not overpaying for quality. Axon’s cloud software and non-lethal weaponry give it durable cash flow potential that could justify its high valuation.

I’ve seen this story before—when strong companies get undervalued for moderate growth, while other firms get inflated on unproven potential. If Axon performs even slightly better than expected, investors could be handsomely rewarded.

Axon Enterprise is highly valued relative to both its free cash flow and earnings, indicating strong investor confidence, but also a premium price. While its leading market position and AI-driven innovation make it an attractive investment, investors should be cautious about whether Axon can deliver growth that justifies these high valuation multiples.

Discounted Cash Flow Significantly overvalued:

Market expects 24.5% growth, yet Axon trades at a 51% premium.

Based on our analysis Axon needs 36% growth to justify its current valuation.

Historically, Axon’s free cash flow grew by 26.2% and revenue by 30% on average.

Real-World Implications

There’s a clear mismatch between the market’s optimism and Axon’s proven growth.

In my own experience, companies priced for perfection often face intense pressure to deliver.

Bottom Line

Axon appears overvalued unless it achieves significantly higher growth than it has historically.

Investors should monitor both free cash flow and revenue trends to gauge whether Axon can close this premium gap.

Does Axon Enterprise Have a Strong Balance Sheet?

Axon Enterprise maintains a strong balance sheet with solid liquidity, low leverage, and disciplined capital management — critical for a company scaling both hardware and software operations.

💵 Operating Cash Flow to Total Debt: 60%

What It Means: Axon generates about 60% of its total debt in operating cash flow, indicating moderate coverage but not a surplus. While this suggests the company can meet many of its obligations, it may still rely on external funding for larger investments or unexpected expenses.

Why It Matters: A solid, though not overwhelmingly high, cash-to-debt ratio provides some flexibility to pursue innovation and strategic goals. However, prudent debt management remains essential to ensure Axon stays resilient in the face of market fluctuations.

📈 Interest Coverage Ratio: 17.6x

What It Means: Axon can easily meet its interest obligations, thanks to consistent earnings and low financial leverage.

Why It’s Notable: A high ratio means minimal financial stress and confirms that Axon is not overly reliant on borrowing — important for a tech company navigating growth, R&D, and expanding global operations.

💰 Free Cash Flow to Total Debt: 45.01%

What It Means: Axon generates enough free cash flow to comfortably cover its debt — suggesting healthy capital structure and conservative financing.

Why It’s a Strength: In a sector where CapEx is necessary for scaling and product development, this ratio shows that Axon isn’t over-leveraged or financing growth with risky debt.

🧾 Goodwill / Total Assets: 16.91%

What It Means: Axon’s goodwill remains modest, indicating a disciplined M&A strategy.

Why That’s Important: Unlike many tech firms that grow by acquiring aggressively (and risk overpaying), Axon appears to have taken a conservative approach to acquisitions, keeping its balance sheet clean and reducing the risk of write-downs.

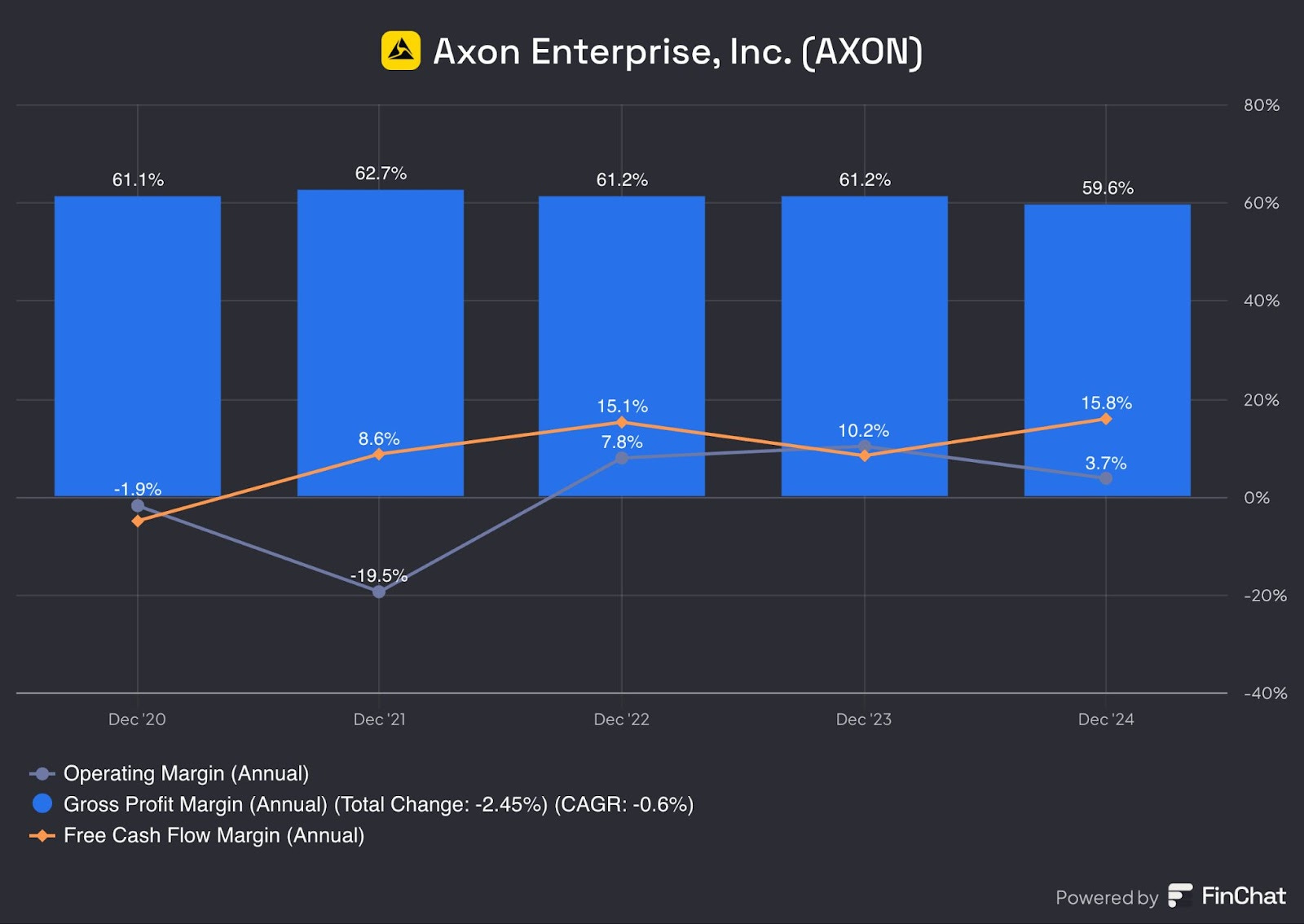

Does Axon Enterprise have Profitable Margins?

🧮 Gross Margin: 59.6% (5Y Avg)

What It Shows: Strong pricing power and efficient delivery of hardware and software solutions.

Why It Matters: Axon earns a sizable profit before expenses — a sign of product-market fit, brand strength, and growing demand in public safety tech.

My Take: Few companies in the defense-tech or SaaS-adjacent space maintain margins this wide. It’s a signal of real operational leverage and moat.

⚙️ Operating Margin: 3.7% (5Y Avg)

What It Shows: Profit after core expenses (pre-tax & interest).

Why It Matters: Axon’s operating efficiency is improving — it’s now earning ~$0.04 per $1 of revenue, and reinvesting heavily in R&D and product development.

My Take: For a company building both hardware (TASERs, cameras) and software (Axon Cloud), any positive margin here shows discipline and future scalability.

💵 Free Cash Flow Margin: 15.8% (5Y Avg)

What It Shows: Cash left after reinvesting in growth and operations.

Why It Matters: Axon is self-funding growth — it can expand, acquire, or innovate without relying on debt or dilution.

My Take: As an investor, a strong FCF margin is gold. It gives Axon the fuel to keep building its platform, reward shareholders, and weather volatility.

⚠️ But... Pressure’s BuildingMargins are tightening. Increased R&D, scaling international sales, or rising cloud costs might squeeze profitability short-term.

Final Thought: Margins tell the deeper story. Axon’s track record is solid — but watch the trajectory. In fast-growth tech, margin compression can be an early warning, or a strategic investment in future dominance.

Is Axon Enterprises Stock Options Tied To Management Performance Rather Than Organisation Performance?

✅ Stock Options & Performance: Axon’s executive stock awards—especially the CEO Performance Award—hinge on company-wide targets like revenue, Adjusted EBITDA, and share price milestones. It’s not purely a personal “manager vs. organization” measure. In my experience, that’s fairly standard: it ensures leaders’ incentives move in sync with overall shareholder value.

✅ Real-World Takeaway In essence, Axon’s equity plans are designed so that leaders benefit only if the broader organization hits critical growth and valuation targets—a powerful motivator for driving results while aligning with shareholder interests.

✅ Stock Options Are Expensed→ Recognized as a real cost over time — no accounting gimmicks.

✅ Performance-Based?→ Yes. Axon ties equity awards to company-wide goals, not just individual executive benchmarks.→ Metrics often include total shareholder return, operational milestones, and long-term growth targets.

✅ Aligned with Shareholder & ESG Goals?→ Absolutely. Axon’s board factors in strategic alignment, risk management, ethics, and ESG progress — especially given its role in public safety tech.

📊 Institutional Support & Market Confidence

Major Investors: Vanguard, BlackRock, and Baillie Gifford — signaling conviction in Axon’s long-term mission.

Stock Performance: Axon has outperformed the S&P 500 over the past 5 years, reflecting investor confidence in recurring revenue, cloud dominance, and public safety tailwinds.

Capital Allocation: Instead of dividends, Axon reinvests heavily in AI, VR, and cloud platforms, favoring long-term value creation.

🧾 Key Compensation Metrics – Axon Enterprise

90% of CEO compensation is performance-based

Stock incentives are tied to key drivers like revenue growth, profitability, and innovation in AI & cloud platforms

Restricted Stock Units (RSUs) are used to promote long-term executive retention and alignment with shareholder interests

👉 This structure ensures that management incentives are directly linked to Axon’s strategic performance, keeping leadership focused on sustained growth, product innovation, and long-term value creation.

Risks and Threats Axon Enterprise Faces

Axon is a high-growth, high-expectation company operating in a complex and sensitive space. It faces risks not just from markets and competition, but also from regulation, social dynamics, and public perception. Managing these effectively is critical to maintaining its moat and justifying its premium valuation.

⚠️ Top Risks

🔐 1. Regulatory & Legal Risks

Government contracts are a major revenue stream. Any changes in law enforcement policies or political sentiment around policing and surveillance tech could impact Axon's sales.

💰 2. Valuation & Market Expectations

If growth slows or margins compress, the stock could correct sharply, as expectations are already sky-high.

🧠 3. Innovation Risk

Failure to outpace competitors or deliver new features could stall growth, especially in a rapidly evolving public safety tech landscape.

💼 4. Customer Concentration

Loss of a major contract or budget cuts at federal/state levels could significantly affect revenue.

🌍 5. Geopolitical & International Expansion Risk

Potential export controls or restrictions on law enforcement products

⚙️ 6. Supply Chain & Manufacturing

Although Axon is a tech company, it manufactures physical products, meaning:

Chip shortages

Supply chain disruptions

Rising input costs

🧾 7. Reputation & Public Sentiment

Axon operates in the highly sensitive area of policing, justice, and civil rights.

Any scandal, product misuse, or negative media (e.g., excessive force incidents tied to TASER use) can rapidly erode public and institutional trust.

⚔️ 8. Competitive Threats

Competitors like Motorola Solutions, NICE, and body cam startups may undercut pricing or offer better integrations with law enforcement platforms.

Big tech (e.g., Amazon Web Services, Palantir) could push into cloud-based evidence management or public safety AI, posing a long-term threat.

✅ Axon’s Playbook

Diversification Strategy:

Axon is expanding internationally (UK, Australia, Canada) and into adjacent verticals like fire departments and corrections.

First-Mover Advantage & Brand Trust:

Axon has established itself as the gold standard in body cams and TASERs, with decades of field data and law enforcement trust.

Customer Feedback Loops:

Axon works closely with law enforcement agencies to co-develop features and improve product-market fit, reducing product risk.

Closed-Loop Ecosystem: Axon Cloud integrates hardware, software, and evidence management — making it harder for clients to switch to competitors

Conclusion

Axon Enterprise has evolved from a TASER-centric venture into a mission-driven public safety technology powerhouse, weaving together hardware, AI, and cloud solutions under the guidance of founder-CEO Rick Smith—who, with a 4% stake worth $1.8 billion, aligns closely with shareholder outcomes. Despite historically weak capital allocation (3.2% ROIC over five years), recent figures reflect a climb in returns (19.1% ROE by 2024). Valuation expectations remain high, with the stock priced for roughly 36% growth — above its ~26% historical average. The company’s strong balance sheet shows manageable debt coverage, though it lacks a deep cushion for unforeseen expansions. Meanwhile, a $129B total addressable market and only 15% U.S. penetration underscore Axon’s growth runway, and the sticky, subscription-based business model has helped it outperform many tech peers. Still, investors should be wary of regulatory flux, potential competitive encroachment, and the challenge of sustaining improvements in capital returns that justify Axon’s premium pricing.

SCC view: Underweight

![Buy [O

Overweight

Hold [-]

Underweight](https://substackcdn.com/image/fetch/$s_!HCt8!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F4721d102-714d-4736-bf49-387a8516a672_247x164.png "Buy [O

Overweight

Hold [-]

Underweight")

Take Your Investments to the Next Level! We provide in-depth, research-driven insights on the leading companies shaping tomorrow’s wealth landscape—spot future leaders and grow your portfolio with us.

Risk Disclosure: This content is for informational purposes only and does not constitute investment advice. Investing carries risk, including potential loss of principal. Always consult with a professional financial advisor to evaluate your risk tolerance and financial goals before making any investment decisions.

Check out our website for more related posts: www.silvercrosscapital.com