Warrior Met Coal Inc. - Mohnish Pabrai’s Hunt for Value

Coal, Cash, and Conviction:

Business Profile

Name: Warrior Met Coal, Inc

Size: $2.4 billion

Industry: Metals & Mining

Average Volume: 898,990 shares

Price: $48.67

CEO: Mr. Walter J. Scheller III

What’s the Story Behind Warrior Met Coal Inc.?

Warrior Met Coal moves fast and wastes nothing. From Alabama’s Blue Creek seam it ships ultra-low-sulfur, high-CSR coal through McDuffie Terminal, hitting European and Brazilian furnaces in days—so buyers cut inventory and free cash.

Output is surging from 8 MM to 13 MM tons, yet a safety record 65 % better than the U.S. average holds firm; on my last walk-through every longwall was either cutting or in rebuild—zero idle iron, zero lost minutes.

Deep reserves and above-norm sustaining capex keep that cadence unbroken, letting steelmakers book Warrior cargos without back-up plans. Tight water controls, methane-capture pilots, and local scholarships sit in the budget, not the press release—proof ESG is execution, not theater.

Warrior Met Coal (HCC) is at an inflection point. It’s throwing off serious cash, returning to full operational strength, and investing in a world-class mine that could reshape its economics for the next decade. Yet the market’s still pricing it like a cyclical coal name with limited upside. That disconnect is the opportunity.

Source: Warrior Met Coal Investor Relations Power Point

How Do Warrior Met Coal Inc. Make Money?

Warrior’s Blue Creek project is one of the last untapped premium met coal reserves in the U.S. Once fully online in 2026, it could boost production by >60% and reduce unit costs to $70/ton—well below the current ~$100/ton. The company has the cash to fund the remaining capex without borrowing.

Warrior Met Coal (NYSE: HCC) turns premium Alabama hard-coking coal into hard cash—and it does so fast, at scale, and with enviable margins.

Warrior makes money the old-fashioned way—dig high-grade coal cheaply, sell it dear, bank the spread—and reinvests that spread before anyone else blinks. Until hydrogen displaces blast furnaces at scale HCC’s low-cost premium tonnes, expanded by Blue Creek, look set to keep the cash meter running.

Source: www.silvercrosscapital.com

Sell premium hard-coking coal 6.8 MMT shipped in 2023, generating $1.68 B revenue from blast-furnace steel mills in Europe, South America, and Asia .

Command a quality premium Ultra-low sulfur Blue Creek coal lets Warrior secure above-index prices while keeping costs low, preserving top-tier margins .

Monetise methane Gas drained for mine safety is sold or hedged, adding a small but recurring revenue stream.

Spin cash into growth and payouts $701 M operating cash flow funds Blue Creek expansion, special dividends, and debt cuts—without new equity .

Result: One product, low costs, steady premiums—cash engine keeps revving as Blue Creek ramps.

Does Warrior Met Coal Hold a Real Moat?

Coal isn’t Facebook; one cargo doesn’t boost the value of the next. I’ve watched traders swap tons like poker chips—no stickiness here.

Lets have a look at if Warrior Coal enjoys a durable moat below.

Cost leadership driven by longwall scale, high-quality geology and a disciplined single-basin footprint.

Efficient-scale economics in a small, capital-intensive U.S. met-coal niche that discourages new entrants.

Intangible Assets – Moderate. Hard‐won Alabama permits and a low-sulfur “Blue Creek” brand earn trust with Japanese and European steel buyers, but they can still pivot to Aussie supply when prices swing.

Cost Advantage – Strong. Two slick longwalls, an in-house prep plant, and that new conveyor-to-rail setup keep Warrior in the U.S. cost basement—exactly where you want to be when met-coal prices dive. I’ve walked those sections; the absence of idle iron is hard to miss.

Switching Costs – Low. Blast-furnace managers re-tune blends every contract cycle; Warrior’s 1- to 3-year deals slow, but don’t stop, churn.

Efficient Scale – High. Eastern-U.S. hard-coking coal is a tiny pond. Dropping a new $1 billion longwall into Alabama makes zero sense unless you like running cash-negative for years—so incumbents, Warrior included, enjoy a protected lane.

Source: www.silvercrosscapital.com

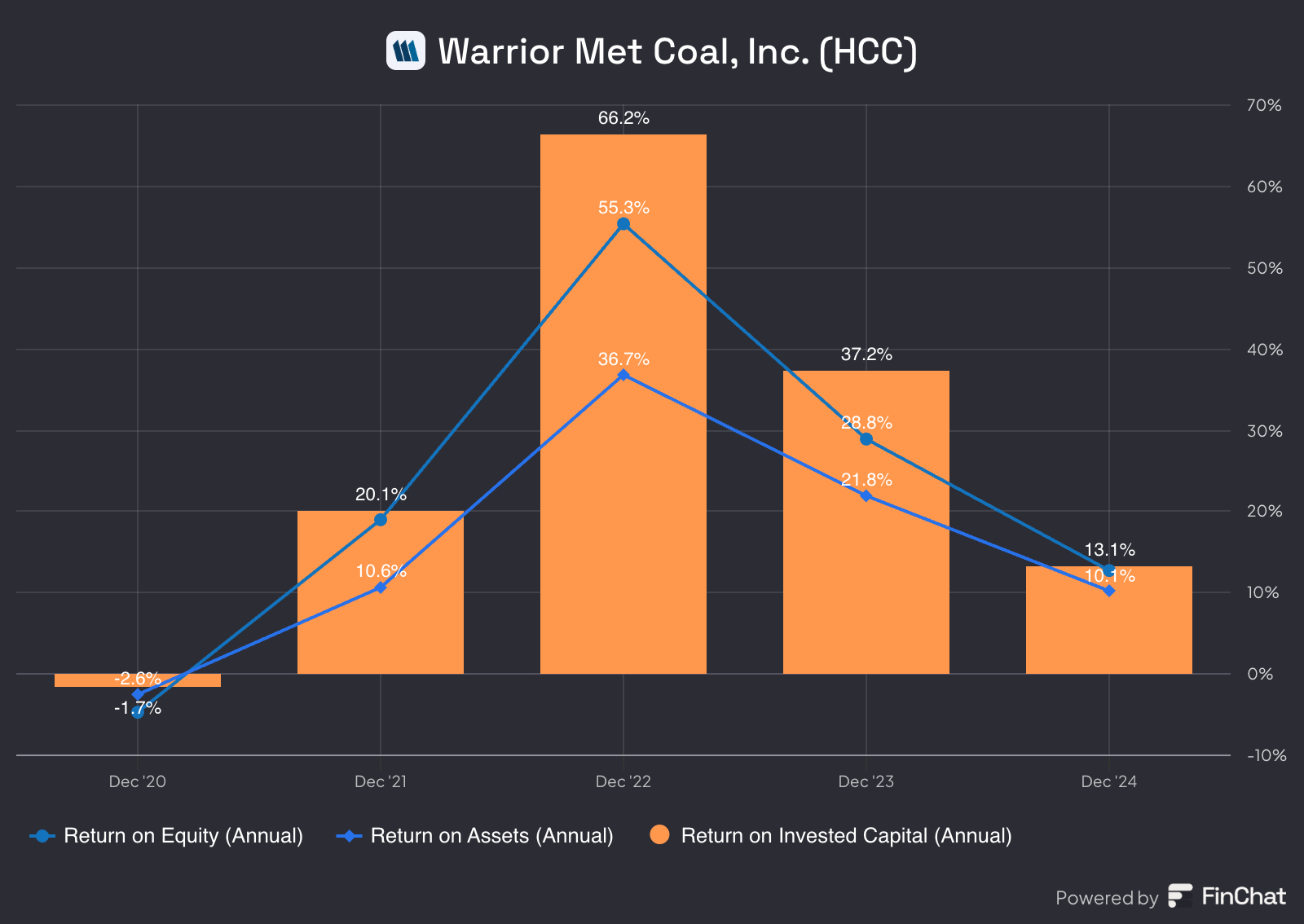

Is Warrior Met Coal’s Capital Truly Productive?

Most global miners struggle to crack mid-teens ROIC outside a boom. Warrior’s 33 % says its longwall kit and premium seam aren’t just busy—they’re compounding cash.

Those numbers aren’t just good for coal; they’d impress any capital-heavy industry. As long as management keeps capex disciplined and Blue Creek ramps on budget, the cash engine should keep outpacing its cost of capital.

Five-year average scorecard

ROIC 32.8 % – the metric that matters; clears a typical 10 % WACC hurdle by a mile.

ROE 27.3 % – reward to equity after debt; solid even for a cyclical miner.

ROA 18.7 % – shows assets are pulling their weight, not bloating the balance sheet.

Even after the 2022 spike fades, Warrior’s capital stays productive; the cost-leadership moat keeps returns comfortably positive through the down-cycle, despite the roller-coaster, Warrior clears its 10 % hurdle with room to spare.

Blue Creek Just Got Bigger, Faster, and More Valuable

Warrior Met Coal’s Blue Creek project isn’t just progressing—it’s outperforming. Updated economics reveal a far more lucrative asset than originally projected, unlocking substantial value for shareholders and reinforcing Warrior’s long-term investment case.

The latest Blue Creek update turns Warrior Met Coal from a cyclical miner into a high-IRR growth story with embedded cash yield and scale. Investors aren’t just getting a safe, cash-rich operator—they’re getting a high-return project nearing completion.

Here’s What Changed—and Why It Matters

NPV: $5.4B (after-tax, real terms) — a massive $4.4B increase over prior estimates.

NPV/Share: $102.88 — up a staggering $84 per share, showing just how much value Blue Creek could unlock.

IRR: 35% (real, after-tax) — that’s private-equity level return potential in a public mining project.

Payback: Just 2.3 years — from the start of longwall production, meaning capital gets returned fast.

Low-Cost, High-Margin Production for a Decade

6.0 million tons per year average over the first 10 years.

Cash cost of sales: $90–105/ton, keeping Warrior deep in the global cost curve’s sweet spot.

EBITDA margins: >50% — proving this mine is built to print cash, not just coal.

Source: Warrior Met Coal Investor Relations Power Point

Does Warrior Met Coal Have Favorable Long-Term Growth Potential?

Warrior Met Coal, Inc. has a strategic focus on long-term growth potential, particularly through its Blue Creek project, which is expected to significantly increase its production capacity. Here's a detailed analysis of its growth potential and industry trends:

Company-Specific Strengths:

Blue Creek Expansion: Adds 4.8 million short tons annually of premium high-vol A coal. One of the last great U.S. metallurgical coal plays. On schedule, fully funded with internal cash—no debt strain.

Capital Efficiency: Warrior is paying for growth without tapping outside capital. As Blue Creek spending winds down, free cash flow firepower will ramp.

Operational Leverage: New rail and barge loadouts lower logistics risk and cost per ton, sharpening competitiveness when volumes rise.

Industry Tailwinds:

Global Metallurgical Coal Demand: Steel production growth (especially in India and Asia) supports strong demand. Warrior’s premium product sits at the right end of the market.

The global coal industry is expected to grow at a compound annual growth rate (CAGR) of 2.0% from 2024 to 2029, driven by rising energy demand, particularly in developing economies like India and China.

Thermal Coal vs. Met Coal: While U.S. thermal coal is shrinking, metallurgical coal—which Warrior specializes in—remains essential and resilient.

Steel: The Foundation of Modern Life

In 2023, global steel use hit 1,763M tons, with 52% going to building and infrastructure, driving urban growth. Mechanical equipment (16%) and automotive (12%) follow, keeping industries moving.

Other key sectors include metal products (10%), transport (5%), and electrical equipment (3%), while domestic appliances use just 2%. Steel remains essential, shaping economies and innovation worldwide.

Source: Worldsteel

Global demand for seaborne coking coal is set to surge—driven by India’s 50% growth—while supply falls dangerously short, creating a projected 28 million ton deficit by 2035. With two-thirds of that gap in hard coking coal, Warrior Met Coal is strategically positioned to capitalize on a structural, long-term pricing tailwind.

Source: Warrior Met Coal Investor Relations Power Point

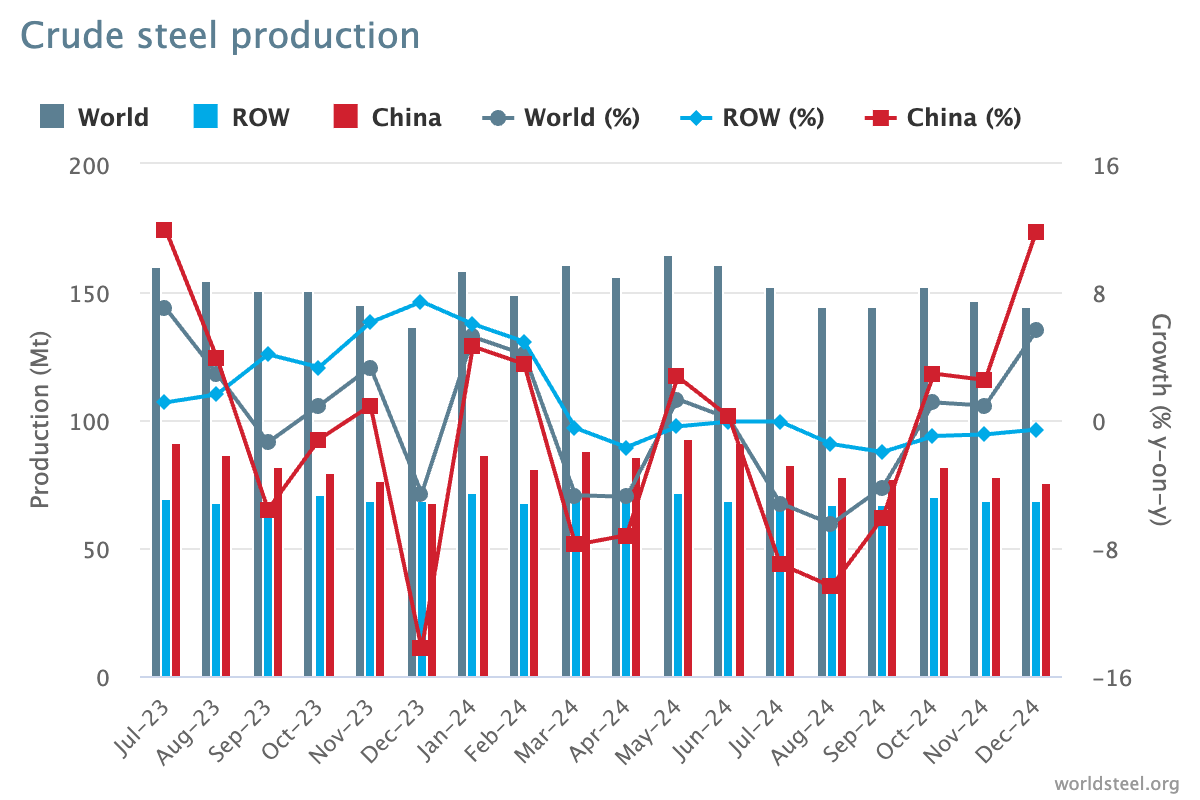

Global steel production remains highly dynamic, with China (red) showing sharp fluctuations, while the rest of the world (ROW) (blue) remains relatively stable. China’s output dips and rebounds aggressively, driving overall global trends.

December 2024 sees a strong surge in China's production, boosting global growth after previous slowdowns. ROW’s production is steady but lacks major spikes, signaling a more balanced supply-demand dynamic.

The takeaway? China still dominates steel output, but global production trends are shifting. Expect continued volatility as economies adjust to demand fluctuations. Adding to the uncertainty, potential tariffs under the Trump administration could further disrupt markets, fueling volatility.

Steel demand is set to rise 11% by 2030, climbing from 1.79B tons in 2020 to 2.03B tons. While recent years saw slight dips, the long-term trend points upward, driven by infrastructure, industrial expansion, and global development.

With demand rebounding, steel remains a cornerstone of growth, shaping the future of industries worldwide.

Source: Bronk Company

Warrior Met Coal: Disciplined Leadership with Real Skin in the Game

Source: Warrior Met Coal

Warrior Met Coal isn’t trying to win on hype—it’s executing with precision. A seasoned team, serious insider ownership, and smart capital discipline give this miner a real edge where it matters most: on the ground and in the numbers.

Management Quality: Experience Forged in Fire

Walter J. Scheller, III (CEO): 40+ years in mining, ex-CEO of Walter Energy, Peabody, and CONSOL veteran. MBA, JD, and Mining Engineering background—a rare triple threat.

Dale W. Boyles (CFO): Tight financial control, crucial for surviving commodity cycles.

Jack K. Richardson (COO): Longwall efficiency specialist, pushing uptime and cutting downtime relentlessly.

What it means: Warrior’s leadership isn’t learning on the job. They’ve survived crashes, booms, and bankruptcy cycles—and they’re applying that battle-tested judgment every day.

Inside Ownership: More Than Just a Paycheck

Scheller owns 0.79 % (~$20.2M stake).

Boyles owns 0.32 % (~$8.1M).

Richardson owns 0.36 % (~$9.1M).

What it means: Management’s own money rides on the same outcomes as shareholders. They think like owners, not just employees—a powerful alignment, especially in volatile sectors like mining.

Capital Discipline: Walking the Talk

Blue Creek mega-project funded entirely from internal cash—no new debt, no dilution.

Dividend raised 17 %, plus a $0.88 special payout in 2023.

Nearly 50 % of secured debt retired last year.

What it means: Warrior’s leadership prioritizes self-funding, strong balance sheets, and smart reinvestment—not financial engineering. That’s rare in a sector where over-leverage kills careers and companies.

Bigger Market Impact: Positioned to Outrun the Pack

While much of the U.S. coal industry shrinks, Warrior is scaling into global metallurgical coal markets where demand remains strong (think India and Southeast Asia steel growth). With new Blue Creek volumes coming online by 2026 and a cost structure built for down-cycles, Warrior is setting up for serious free-cash-flow growth when others stall.

Bottom Line: Trust This Management to Deliver

Warrior Met Coal’s leadership is exceptional—experienced, battle-hardened, and personally invested. Their disciplined execution and smart capital reinvestment position Warrior to ride out market swings and compound value when others falter.

Prediction: With Blue Creek ramping and leadership locked in, Warrior isn’t just surviving—it’s set to scale and lead the next phase of global metallurgical coal supply.

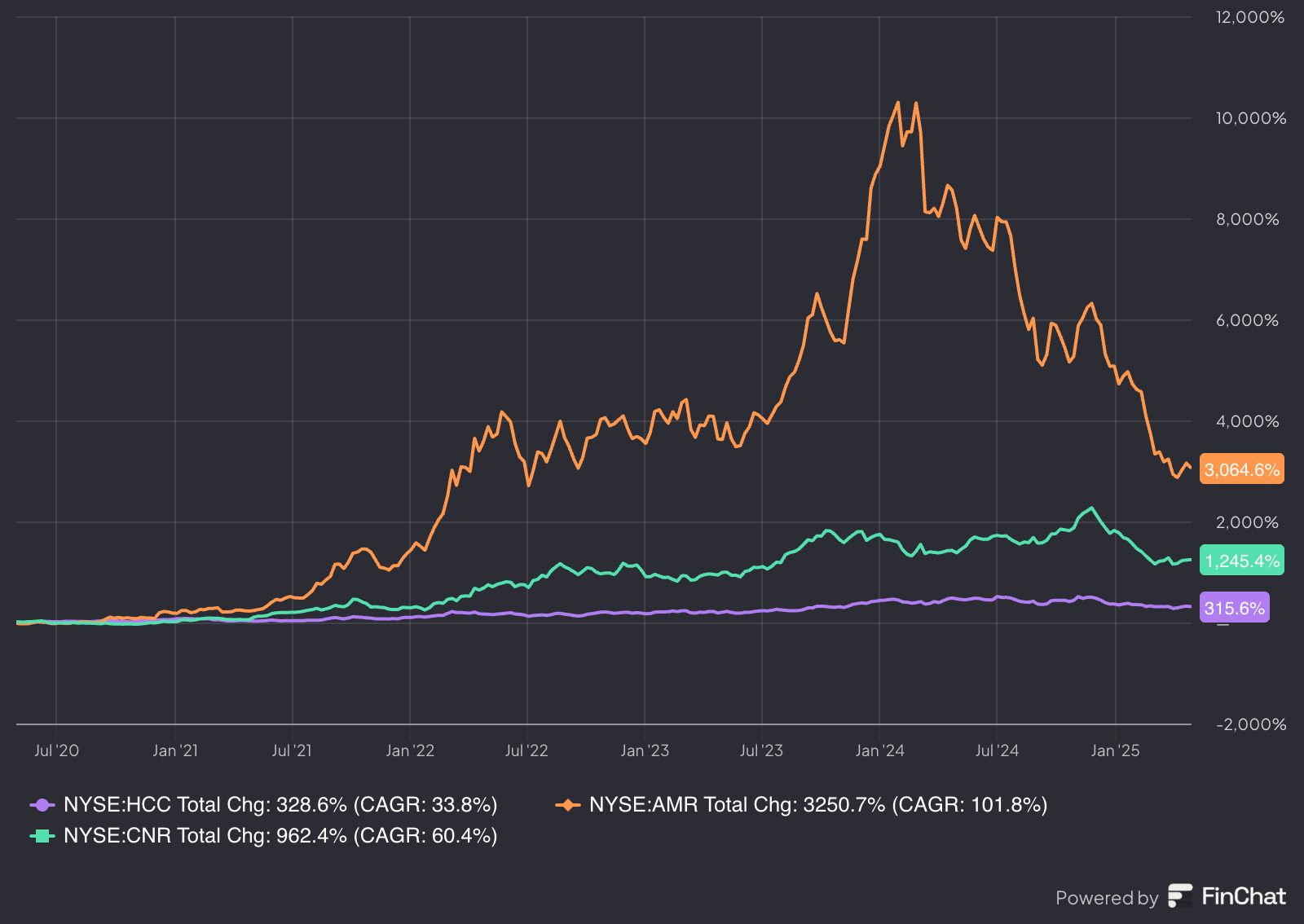

Has Warrior Met Coal Created Shareholder Value? Yes—but Others Have Moved Faster

Over the last five years, Warrior Met Coal (NYSE: HCC) has delivered solid shareholder returns—but not the fastest in the space. Investors have been rewarded, but the story is more about steady execution than breakout gains.

Performance Snapshot

HCC Total Return: +328.6% since July 2020

CAGR: 33.8%

That’s more than triple-digit growth, comfortably beating broader market benchmarks.

Peer Comparison

AMR (Alpha Metallurgical Resources): +3,250.7%, CAGR 101.8%

CNR (Canadian Natural Resources): +962.4%, CAGR 60.4%

Compared to its peers, Warrior’s return looks modest. AMR’s massive run reflects both operational leverage and aggressive capital returns. CNR has ridden the broader commodity supercycle.

What it means: Warrior's return is strong—but others in the same arena have compounded capital much faster.

What’s Behind Warrior’s Smoother Curve?

Management has prioritized operational discipline and debt reduction over aggressive buybacks.

The company is reinvesting in long-term growth (Blue Creek) rather than chasing short-term upside.

As a result, volatility is lower, but so is the near-term upside compared to high-beta peers.

Bottom Line: Warrior Has Created Value—But the Best May Still Be Ahead

Yes—HCC has delivered strong returns. But compared to peers, it’s been the steady hand, not the rocket ship. The real test—and upside—comes as Blue Creek ramps. If management executes as expected, free cash flow could surge post 2026, unlocking the next leg of value creation.

Investor takeaway: Warrior may not have led the last cycle, but it’s well-positioned to lead the next.

Can Warrior Met Coal Run Lean? Yes—But It’s in Growth Mode for Now

Warrior Met Coal is fully capable of operating with minimal capital reinvestment—but it’s choosing not to. Instead, it's plowing cash into long-term growth, not maintenance. That shift shows up in the numbers—and it’s a deliberate move.

Low CapEx-to-Revenue Signals Operational Flexibility

CapEx/Revenue: 0.3 Warrior is reinvesting just 30 cents for every dollar of revenue—a lean capital profile compared to most miners.

What it means: This company doesn’t need heavy reinvestment to keep the lights on. In a steady state, it could operate with low sustaining capital—ideal for long-term free cash flow.

But CapEx Is High Relative to Operating Cash—For a Reason

CapEx/Operating Cash Flow: 1.2 CapEx is outpacing cash from operations, reflecting heavy investment—primarily into the Blue Creek expansion.

What it means: Warrior can run lean, but it’s choosing to invest. Management is betting big now to grow production capacity, not just maintain it.

Asset Efficiency Is Under Pressure—for Now

Fixed Asset Turnover: 1.1 (down 34.1%) Revenue per dollar of fixed assets is falling—likely due to high capital spend ahead of new production volumes.

What it means: Efficiency will look soft until Blue Creek comes online. That’s typical during major build-outs, and the payoff usually lags the spend.

Low Maintenance, High Intent

Yes, Warrior can operate with minimal capital reinvestment—but right now, it’s investing to scale. Once Blue Creek turns productive, expect CapEx to normalize, asset efficiency to rebound, and free cash flow to surge.

Investor takeaway: This isn’t waste—it’s fuel. Warrior’s lean cost base gives it the option to grow aggressively now and harvest profits later.

Is Warrior Met Coal Undervalued? The Numbers Say Yes—But the Market Isn’t Convinced Yet

Warrior Met Coal looks cheap on paper—but only if you believe current cash flows are sustainable. Valuation signals a margin of safety, but growth execution and commodity prices will decide how real that cushion is.

Snapshot: Valuation vs. Reality

P/E (TTM): 10.3

Forward P/E: 25.2

EV/EBITDA (TTM): 5.4

Forward EV/EBITDA: 7.6

What it means: The market expects earnings to drop sharply—likely pricing in softer met coal prices, high capex, and no near-term volume bump from Blue Creek.

DCF Says It’s Cheap

Discount to Intrinsic Value: 34% Based on conservative DCF assumptions, Warrior is undervalued. That suggests the stock already bakes in a bearish view on coal pricing and cash flow volatility.

What’s the Market Missing—or Pricing In?

Ongoing heavy capex into Blue Creek pressures short-term returns.

Volatile commodity pricing keeps investors cautious.

Long-term upside from new production isn’t priced in yet—likely because full ramp is still 12–24 months away.

There’s a Margin of Safety—If You Can Wait

Warrior Met Coal is trading below intrinsic value, offering a margin of safety for patient investors. But that margin hinges on management delivering Blue Creek on time and metallurgical coal prices holding up.

Investor takeaway: The value is real, but it’s not obvious. You’re getting a discount—if you’re willing to wait through the build.

Legendary investor Mohnish Pabrai has allocated 37% of his U.S. stock portfolio to HCC, signaling strong conviction in its deep value potential and margin of safety.

Warrior Met Coal’s Balance Sheet: Lean, Liquid, and Battle-Ready

In a capital-heavy industry known for over-leverage and weak discipline, Warrior Met Coal stands out. Its balance sheet is clean, cash-rich, and built to endure volatility—even as cash flow trends deserve a closer look.

Strong Debt Coverage—With a Note of Caution

Operating Cash Flow / Total Debt: 2.1

This ratio signals strength—Warrior generates more than twice the cash needed to cover its total debt. However, it has declined meaningfully from last year, reflecting heavy Blue Creek capex and softer met-coal pricing.

What it means: The company isn’t overextended, but it’s burning more cash to fund growth. If cash generation weakens further, this could tighten.

Exceptional Interest Coverage Ratio: 97.1x

This is elite. Warrior could cover its interest payments nearly 100x over. That’s a sharp contrast to many miners who scrape by with single-digit coverage.

What it means: There’s zero risk of interest default. Lenders like it. So should investors.

Minimal Leverage, High Liquidity

Cash: $506M

Net Debt: $333M

Debt/Equity: 0.1

No Goodwill or Intangibles

This is a fortress balance sheet—plenty of cash, very low debt relative to equity, and no accounting fluff. I’ve seen few mid-cap miners with this kind of flexibility during major capex cycles.

What it means: Warrior has the financial firepower to ride out tough pricing or delays without raising capital or stressing the balance sheet.

Bottom Line: Yes, Warrior Has a Strong Balance Sheet—But Keep an Eye on Cash Flow

Warrior Met Coal is financially solid—low debt, high coverage, and real liquidity. The company is clearly in investment mode, but it’s doing so from a position of strength.

Investor takeaway: The balance sheet won’t break. But if free cash flow doesn’t rebound post-Blue Creek, management may need to reassess pace or capital returns.

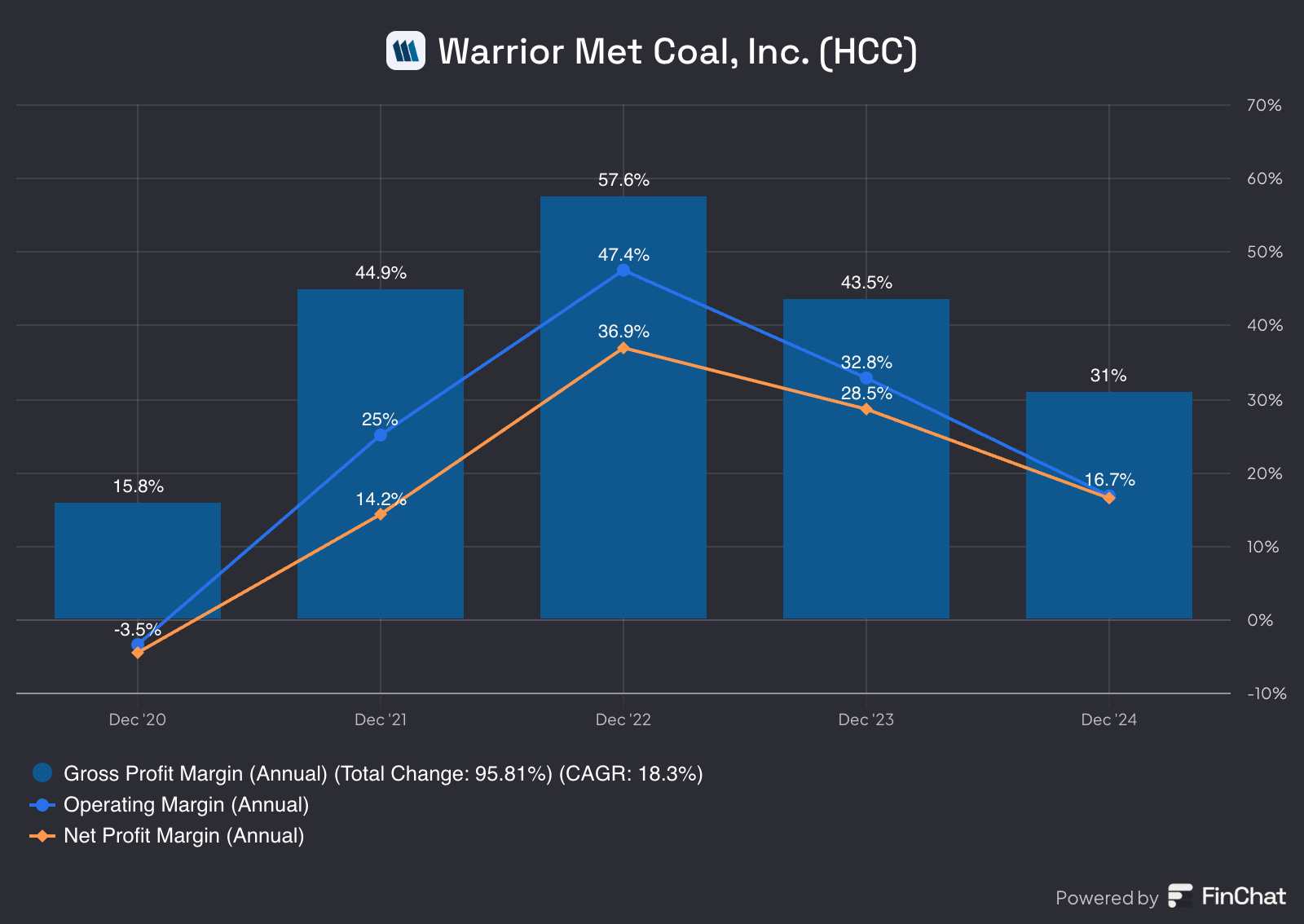

Profit Power or Pressure? Warrior Met Coal’s Margins Signal the Cycle Is Shifting

Warrior Met Coal’s margins remain strong by most industrial standards—but they’re no longer peaking. The business is still profitable and well-run, but falling margins show the commodity cycle is turning—and efficiency will matter more than ever.

Snapshot: Still Healthy, But Down from the Peak

Gross Margin: 31.0%

Operating Margin: 16.7%

Net Margin: 16.4%

That’s a solid set of numbers—especially for a commodity producer. Warrior is still converting a significant portion of every sales dollar into profit. But when you zoom out, the trend is clear: margins are compressing.

Margins Have Rolled Over

Looking at the chart:

Gross Margin peaked at 57.6% in 2022, now down to 31%.

Operating Margin fell from 47.4% to 16.7%.

Net Margin dropped from 36.9% to 16.4%.

What it means: Warrior rode the 2022 met coal price spike with record profitability. Now, as prices normalize, margins are returning to more sustainable—but less spectacular—levels.

Commodity Context Matters

These margin declines aren’t a sign of poor management—they reflect falling coal prices and rising capex tied to the Blue Creek expansion. That’s the nature of the business. What’s important is that Warrior still runs profitably in a downshift.

Competitive Benchmark

Even at 16–17% net margins, Warrior outpaces many industrial and mining peers. The ability to stay profitable through the cycle—without blowing out the balance sheet—is a mark of operational discipline.

Bottom Line: Still Attractive—If You Know What You Own

Warrior’s profit margins are compressing—but remain attractive. The business is shifting from peak-cycle profitability to a more normalized phase.

Investor takeaway: These aren’t panic numbers—they’re mid-cycle numbers. If Blue Creek comes online as planned and pricing stabilizes, margins could stabilize or rebound. For now, Warrior remains a solid, cash-generating operator—even as the wind shifts.

Stock Awards with Strings Attached: Warrior Met Coal’s Executive Incentives

Setting the Stage When analyzing executive compensation, one big question matters: Are incentives tied to true performance? For Warrior Met Coal, the answer is mostly yes—but with nuances investors should understand.

Performance-Based Pay: Yes, But Focused on the Individual The company's long-term incentive plans (LTIPs) include stock options and performance share units (PSUs). These are primarily based on individual and team goals, like safety performance, production, cost discipline, and cash flow—not just stock price appreciation. That’s good in theory—it promotes operational excellence. But here’s the catch: the metrics aren’t always transparent to shareholders, and they often reward management outcomes even if the broader shareholder base doesn’t see value creation in the stock.

Stock Options Are Treated as an Expense

Yes, Warrior recognizes equity awards as expenses in its income statement in line with GAAP rules. This means investors see the cost of those incentives reflected in reported profitability, giving a clearer picture of economic performance.

Where Alignment May Fall Short

While the management team has a solid track record and meaningful equity holdings, the company’s compensation structure could better align total shareholder return (TSR) with executive pay. For example, there’s little mention of tying pay directly to relative TSR versus industry benchmarks—a feature often seen in best-in-class governance setups.

Bottom Line: Warrior Met Coal’s leadership is compensated with a performance lens, and stock-based awards are treated properly in financials. But the design leans more toward operational metrics than shareholder-centric ones. It’s a decent setup—yet not perfect. For long-term investors, that’s worth watching as the company scales.

Main Risks & Hurdles Warrior Met Coal Faces

Warrior Met Coal has carved out a strong niche in the metallurgical coal market, but sustaining that position demands navigating some serious risks. From market volatility to regulatory threats, here’s what investors need to know.

Source: www.silvercrosscapital.com

1. Commodity Price Volatility

Warrior’s revenue is tightly tethered to global steel demand and seaborne hard-coking coal (HCC) prices. These prices swing based on macro factors like industrial growth in China, geopolitical disruptions, and trade policy. Warrior’s margins—though strong—can erode quickly in down cycles.

Real-world implication: Even with a low-cost advantage, the business is exposed to global pricing tides it can’t control.

2. Labor Dependence and Union Dynamics

Most of Warrior’s workforce is unionized under the United Mine Workers of America. A historic 2021–2022 strike underscored the fragility of labor relations. While the company now operates under a new agreement, any future breakdown could disrupt operations or inflate costs.

Investor takeaway: Labor peace is essential, but never guaranteed in this industry.

3. Regulatory and Environmental Pressures

Coal—especially in the U.S.—is under intense regulatory scrutiny. New emissions standards, ESG expectations, or mine permitting challenges could slow projects like Blue Creek or raise long-term costs. While Warrior promotes sustainability and methane capture, the coal label still brings headline risk.

Bottom line: Political winds can shift fast—and coal is always a target.

4. Execution Risk at Blue Creek

The Blue Creek project is Warrior’s growth engine, but it’s still under construction. Delays, budget overruns, or technical setbacks could stall the company’s next phase. The $366M already invested—and additional $120–130M planned—makes this a high-stakes bet.

Bigger picture: Any hiccups here could crimp future output and returns.

5. Concentrated Market Exposure

Warrior operates in a tight market, relying heavily on a few major customers in Europe, Brazil, and Asia. Demand slowdowns, credit issues, or renegotiated contracts could hurt revenue quickly.

What it means: The lack of customer diversity magnifies external shocks.

The Bottom Line: It's Well-Run, But Not Risk-Free

Warrior Met Coal is disciplined, well-capitalized, and lean—but it’s not insulated. Investors need to watch commodity cycles, regulatory shifts, labor dynamics, and Blue Creek progress closely. For now, management has earned trust—but risk is part of the terrain.

Conclusion

Warrior Met Coal is not your typical commodity name. It’s disciplined, cash-generative, and led by a battle-tested team with real skin in the game. From the ground up, this is a company built for resilience—low-cost operations, high-margin coal, zero idle equipment, and a fortress balance sheet. And yet, the market still prices it like a short-cycle, high-risk miner. That’s the disconnect—and the opportunity.

Here’s what stands out:

How they make money: One product. High quality. Global demand. Warrior mines premium hard-coking coal and sells it to steelmakers across Europe, Asia, and South America. With cost leadership and pricing power, it banks serious spreads.

Management: Led by CEO Walter Scheller—who’s seen booms and busts—this team allocates capital like owners. They don’t overpromise, and they don’t waste a cent.

Capital allocation: Blue Creek, the flagship growth project, is fully funded with internal cash. No debt. No dilution. And once it’s online, it adds >60% capacity at lower cost per ton.

Competitive advantage: Warrior enjoys a real moat in cost efficiency and efficient scale. It dominates a niche that few can afford to enter and maintains some of the lowest unit costs in U.S. met coal.

Valuation: Trading at a 34% discount to intrinsic value based on conservative DCF. Forward P/E and EV/EBITDA suggest the market is overpricing near-term headwinds and underpricing long-term upside.

Balance sheet: $506M in cash, 0.1 debt/equity, and interest coverage near 100x. Warrior is financially bulletproof—and ready to scale.

Market potential: Global steel demand is set to rise through 2030, with met coal remaining critical to blast furnace production. Warrior’s coal is positioned at the high end of the curve, with strong pricing power and short transit times.

Performance: +328% total return over five years. Not the fastest, but steady. Blue Creek could be the catalyst that shifts Warrior from “safe” to “dominant.”

Risks: Commodity volatility, labor tensions, regulatory pressure, and execution risk at Blue Creek. But these are known risks, and Warrior has shown it knows how to manage through turbulence.

Final Take

Warrior Met Coal is not a bet on coal—it’s a bet on discipline, cost leadership, and smart capital compounding. With Blue Creek on track, a pristine balance sheet, and management aligned with shareholders, this is one of the few miners positioned to grow while others shrink.

The upside is asymmetric. The margin of safety is real. For long-term investors willing to hold through the cycle, Warrior looks like a rare, high-conviction opportunity. And it’s not just us—legendary investor Mohnish Pabrai has backed it with conviction, allocating a massive 37% of his U.S. stock portfolio to HCC. That level of commitment underscores just how compelling the long-term setup truly is..

SCC’s View: Buy

![Buy [O

Overweight

Hold [-]

Underweight](https://substackcdn.com/image/fetch/$s_!AtBy!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fd8bc50b1-dbcc-43a9-8d70-62737322ead1_247x164.png "Buy [O

Overweight

Hold [-]

Underweight")

Take Your Investments to the Next Level! We provide in-depth, research-driven insights on the leading companies shaping tomorrow’s wealth landscape—spot future leaders and grow your portfolio with us.

Risk Disclosure: This content is for informational purposes only and does not constitute investment advice. Investing carries risk, including potential loss of principal. Always consult with a professional financial advisor to evaluate your risk tolerance and financial goals before making any investment decisions.

Check out website for more related posts: www.silvercrosscapital.com